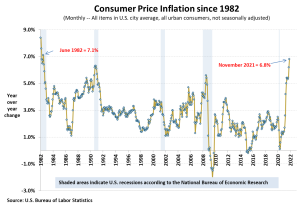

Consumer Price Inflation surged 6.8% in November from year-ago levels, the biggest increase since June 1982.

Interest on Inflation-protected savings bonds (commonly called I-bonds) is linked directly to inflation. The interest rate paid on I-bonds is determined every six months and they are now earning an annualized 7.12%. This rate is available on bonds purchased now through April 30. Given much lower interest rates on other safe investments, they deserve a close look. The roles they can serve in your portfolio and details to be aware of are discussed below.

Roles for I-bonds

- A high yielding emergency fund, after a one-year holding period. I-bond yields are quite attractive to the alternatives. A comparably safe one-year CD earns about 0.65%. Savings accounts at major banks earn next to nothing. A one-year U.S. Treasury bill earns about 0.25%.

- An investment for buying stock funds after the stock market tanks. Periodic drops of 20% or more occur with regularity. I-bonds never decline in value serve as dry powder you can sell to fund those purchases.

- A safe asset that dampens the turbulence of stocks in your total portfolio.

- A secure source of funds to meet essential spending in retirement.

- A backup source of potentially tax-free funding for college expenses. 529 College Savings Plans are more effective for longer horizons because they have high stock allocations at early stages.

I-bond investment details

They:

- require a minimum purchase of $25.

- have annual purchase limits per social security number of $10,000 ($20,000 for a couple).

- If liquidity allows, a couple could lock in the current 7.12% on $20,000 in 2021 and another $20,000 in 2022. 2022 purchases need to be made before the current May 1st inflation rate reset in 2022 to lock in the current 7.12%. Up to $5,000 more can be purchased by directing Federal tax refunds into I-bonds.

- do not decline in value. If deflation occurs, I-bond interest plus any fixed-rate interest rate does not fall below 0.0%. Deflation is rare but occurred in the 2008/09 financial crisis and when oil dropped sharply from 2014 to 2016 as seen in the chart above.

- are free from state and local taxes. Only Federal taxes apply.

- are tax-deferred for up to 30 years, full maturity. You can report interest every year but most wait until they redeem the bonds to take advantage of compounding.

- are purchased without transaction or fund/account management fees through the TreasuryDirect website.

- may earn a fixed rate on top of the variable inflation rate. The fixed-rate stays constant for as long as you own it but is now 0.0% and can be ignored.

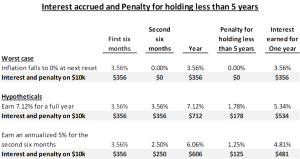

- lose the last 3 months of interest if redeemed (sold) in less than 5 years. Even after a penalty, interest earned for a year will still be far ahead of CDs and other safe alternatives as shown below.

Potential I-bond interest after the 7.12%

I-bond interest rates reset twice a year on May 1st and November 1st. When the interest rate changes and what the rate will depend on when you buy them. The next May 1st rate will be determined by unknown inflation from October 2021 to March 2022:

But October and November 2021 inflation are known: it was 7.14% and 6.50%. Inflation during the next four months is uncertain but is quite likely to remain elevated. This makes I-bonds a superb, but illiquid, investment choice for the next year.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.

")