At a recent Fortune 200 Ernst and Young (E&Y) workshop for employees (and spouses, such as myself), the presenter recommended maintaining an asset allocation suited to one’s goals, resources and tolerance for risk. Known as “Rebalancing,” this is standard advice and makes a lot of sense as described below.

At a recent Fortune 200 Ernst and Young (E&Y) workshop for employees (and spouses, such as myself), the presenter recommended maintaining an asset allocation suited to one’s goals, resources and tolerance for risk. Known as “Rebalancing,” this is standard advice and makes a lot of sense as described below.

However, my ears began to perk up when the presenter additionally recommended rebalancing during “traumatic” market events, not on a specific date each year. Again, this too makes a lot of sense – almost. It may have been a matter of emphasis or the need to get through a lot of material, but the presenter left out an additional couple of critical points that I’d like to add:

- Rebalancing frequency should be tempered so the costs involved don’t overtake the benefits received.

- The discipline required to pull this off cannot be overemphasized.

Understanding rebalancing’s underlying rationale and process is the first step for you to implement the recommendation.

Rationale: risk control and potentially enhanced returns.

- Over time, some of your assets will outperform while others will underperform. If you do nothing in response, your investment mix will eventually drift away from your original targets — far enough away that you may eventually end up with a different portfolio than you planned: either too risky or too “safe” (i.e., lacking expected “future” higher returns “performance”) for your situation.

- Research on whether rebalanced portfolios actually improve returns is mixed due to different time periods studied and methodologies used. A Wall Street Journal article quoted 0.5% over decades.1 A Vanguard study concluded that rebalancing did not affect performance.2 Another study, which monitored different rebalance time frequencies, calculated rebalancing rewards at 0.62%.3

Rebalancing process during “trauma.”

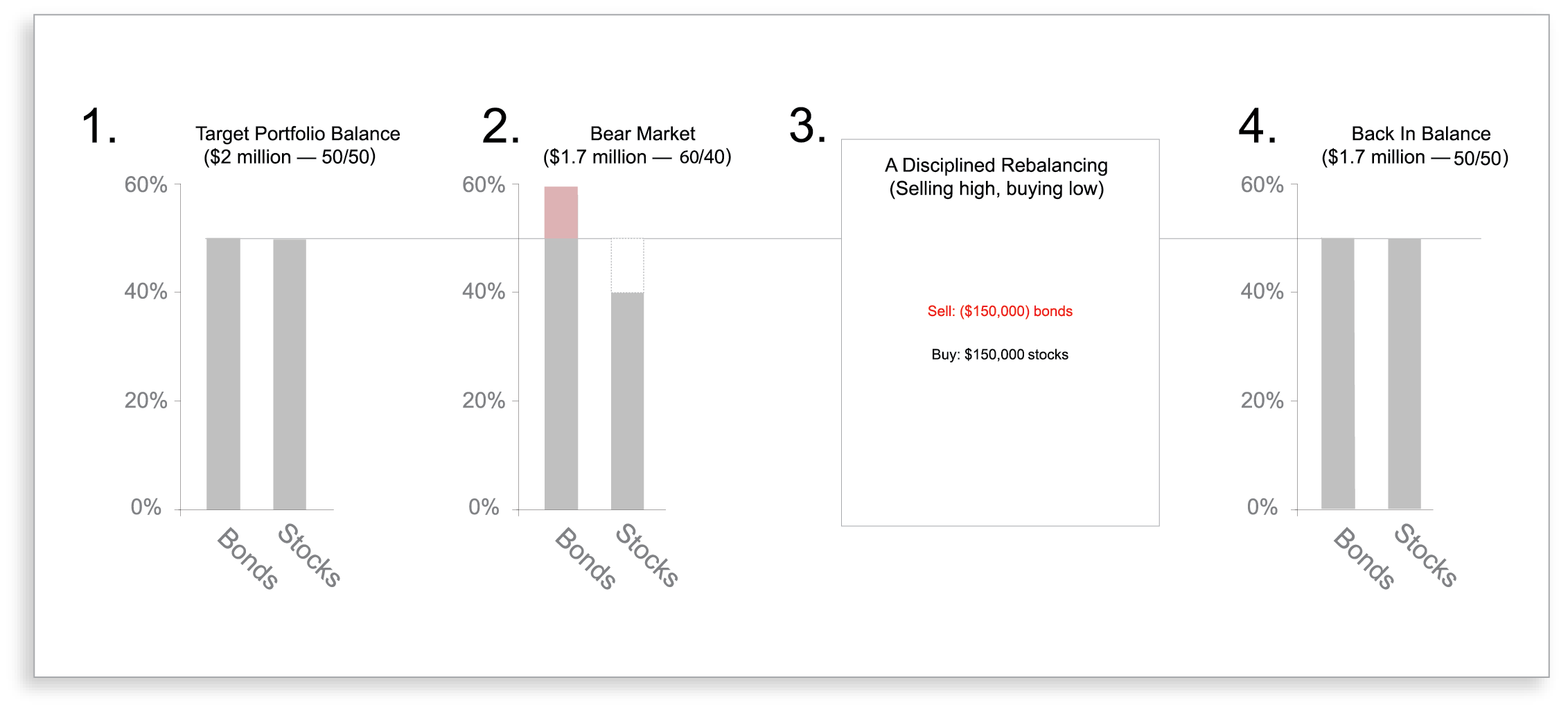

Imagine your target mix is half stocks and half bonds. With a $2 million portfolio this would be $1 million each in both stocks and bonds. Enter a traumatic event for your stocks (or their drawn-out decline). Assume your portfolio is now worth only $1.7 million and the mix is 40% stocks / 60% bonds. To rebalance, $150,000 of the now-overweight bonds are sold and the proceeds buy stocks that have become underrepresented.

Graphically, this represents what happens:

Click to Enlarge

Is it easy to rebalance after such a decline? No way. Buying more of the investment that has declined and selling the investment that has been most stable or even climbed in value requires tremendous self-discipline. The 2008 Global Financial Crisis is the quintessential example. To rebalance then, you had to sell some of your safe-harbor holdings and buy stocks, when stocks looked most dangerous. Those who rebalanced captured available returns during the subsequent recovery. But at the time, it represented a huge leap of faith.

Rebalancing when your portfolio is rising.

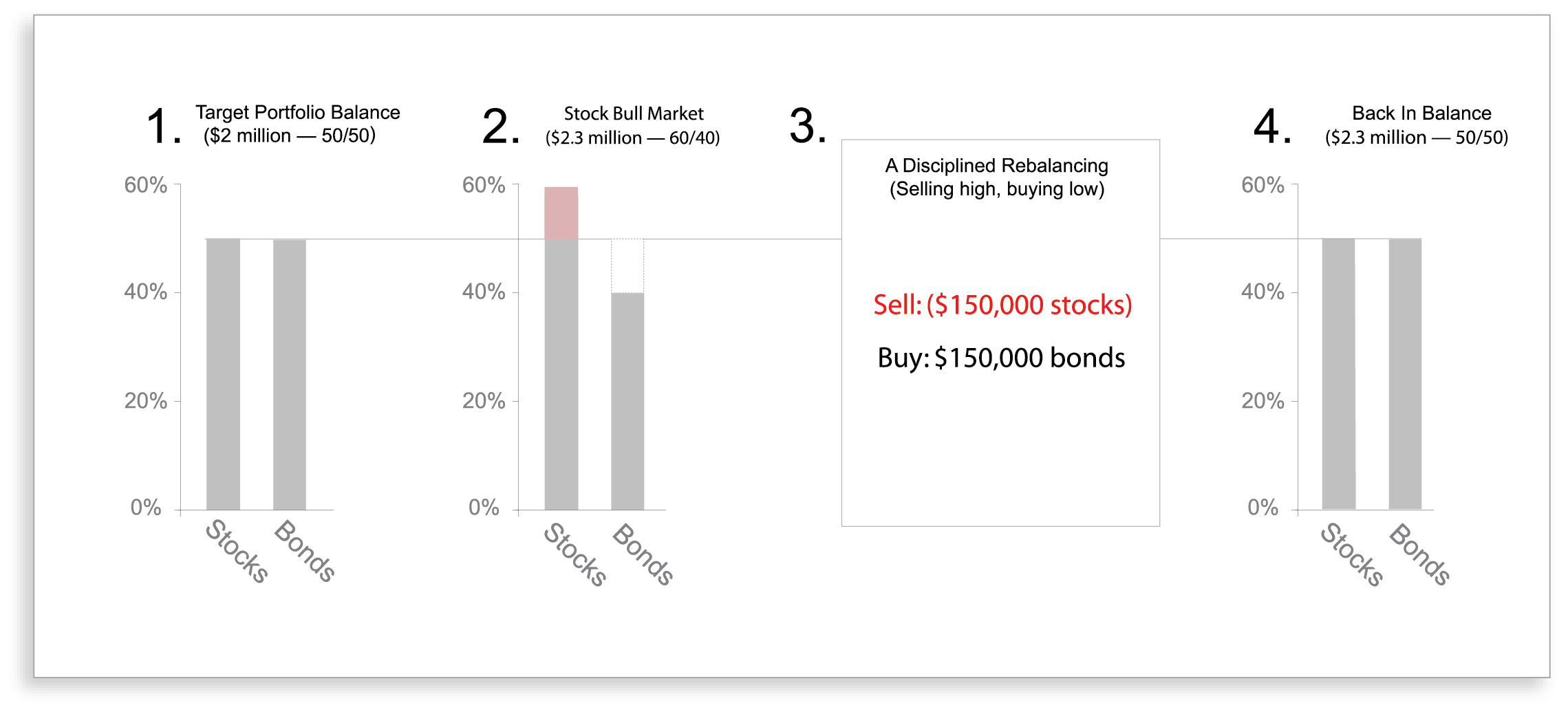

Take the same beginning $2 million portfolio but assume it grows and the mix is 60% stocks / 40% bonds. To rebalance, $150,000 of the now-overweight stocks are sold and the proceeds buy bonds that have become underrepresented.

Graphically, this represents what happens:

Click to Enlarge

Again, this is not easy. Selling the investment that has increased and buying the investment most stable or even declined in value may make you feel alone and foolish. Those who rode the 1990s dot-com wave through its crest or real estate into the lending frenzy prior to 2008 understand why it’s a good idea to control risk by realizing gains.

Costs: always a practical concern.

Trading during rebalancing incurs transaction fees as well as potential tax liabilities. To help us achieve a reasonable, middle ground, we have guidelines for when and how to cost-effectively rebalance. Included among them are:

- Preset rebalancing boundaries for when to buy and sell investment that are wide enough to keep you on target but loose enough to minimize excessive trading (e.g., +/- 10% of a 50% target allocation creates boundaries of 45% to 55%).

- Use any new money added to your portfolio to perform efficient rebalancing whenever possible.

- Strategically “locate” your assets among taxable and tax-deferred accounts so that more of the gains are recognized within your 401(k) or IRA and taxes are reduced. (See: Asset Location, where investments are placed, can reduce taxes).

The Rebalancing Take-Home.

Rebalancing makes a great deal of sense once you understand the basics: It gives you a clear, evidence-based process and effective, low-cost solutions for staying on course toward your personal goals through rocky markets.

At the same time, rebalancing within your portfolio requires both emotional resolve as well as informed management, to ensure it’s being integrated consistently and cost effectively. Helping you periodically rebalance your portfolio is another way Granite Hill Capital seeks to add value.

1 Jason Zweig, Kelsey Hubbard, “’Rebalancing’ Your Portfolio Can Be a Tough Ride,” Wall Street Journal, (March 7, 2009).

2 Colleen M. Jaconetti, Francis M. Kinniry, Jr., Yan Zibering, “Best practices for portfolio rebalancing,” Vanguard research, (July 2010): 12.

3 Gobind Daryanani, “Opportunistic Rebalancing: A New Paradigm for Wealth Managers,” Journal of Financial Planning, issue 1 (January 2008): 11.

[Photo by winnifredxoxo]

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.