In my last blog posting, “Is it Safe?” I provided a solid rationale for diversifying overseas, despite current headlines. Still, an ongoing stream of uncertainty might have you thinking that it’s time to forget about a significant allocation to foreign stocks and funds. Fearful investors tend to flee to more familiar home turf, but I would propose the best defense to global volatility remains a prudent – and yes, still relatively significant – allocation to foreign holdings that reflects your personal risk tolerance.

A pictorial glance at past performance speaks a thousand words on why this is so:

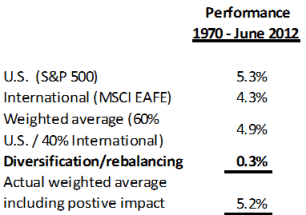

60% S&P 500 / 40% MSCI EAFE (Europe, Australasia, Far East index) rebalanced annually to restore target allocations.

Indexes are not available for direct investment but reveal positive and negative performance over time.

Their performance does not reflect the expenses associated with the management of an actual portfolio.

Data is from sources believed to be reliable but cannot be guaranteed.

Reading the chart

- U.S. and international performances typically move in the same direction, albeit to varying degrees. The 70s are an exception. The U.S. is represented by the S&P 500 (the blue bar), and international performance is represented by MSCI EAFE, the Europe, Australasia, and Far East index (maroon bar).

- International performance helped reduce losses in the 70s and 00s and even enhanced performance in the 80s, but then underperformed in the 90s.

- A portfolio that combines 60% U.S. and 40% international stocks (the gray bar) hugs close to the difference between the two, offering a smoother ride across the 40+ years displayed. In the 70s this portfolio lost .1%, a loss so slight that it barely appears on the chart.

- Long-run performance during this particular timeframe happened to favor the U.S. over international by approximately 1 percent.

Takeaways:

Don’t underestimate how it feels when your international funds underperform.

Home market bias is real, especially if your brother-in-law, neighbor or boss gloats about how well he or she is doing by avoiding international. Consider the 90s: the S&P 500 Index rose nearly 300% in the decade, while MSCI’s EAFE index rose less than 50%. Ouch.

International diversification is expected to deliver a positive impact:

If you scrutinize the entire period, the bars at the far right—the 60/40 portfolio—at 5.2% looks closer to the S&P 500’s 5.3% than it should be. Without diversification and rebalancing, the performance of a portfolio would be a weighted average of the two indexes, or 4.9%. But with them, there is an added positive impact of .3%:

The benefit was between 0.3% and 0.4% for each of the decades prior to the new millennium when it fell to 0.1%. The benefit fell in the last decade with elevated market volatility due to the global economic crisis combined with U.S. and international markets moving more in tandem. For the past couple of years there was no diversification benefit, but it seems likely that as economies heal—albeit slowly and painfully—volatility will decline over time, stocks will stabilize and the diversification and rebalancing benefits will revert to historical norms.

How much?

For most investors, determining an appropriate mix between domestic and international is a balancing act. A minimum of at least 20% of the stock portion of your portfolio seems prudent to capture the positive diversification benefit and protect against catastrophe; however with greater than 50%, diversification and rebalancing benefits begin to decline and increased international investing costs take a greater toll. There are also tax consequences to consider. Foreign taxes will be deducted for dividends and capital gains in the countries where your funds are invested. You may get a credit for these taxes, but they need to be in a taxable account, not an IRA or 401(k) where the credit would be lost.

As with all investment decisions, how much international to hold needs to reflect your personal risk capacity, which boils down to the impact of an unexpected sharp loss. If such a loss puts your lifestyle at risk—and stocks are, after all, more volatile than bonds—it makes sense to dial back on your overall stock investments. But because that risk can occur anywhere, at anytime, it also makes sense to avoid the temptation to throw in the towel right before international recovers (or falls less). Instead, retain your planned allocation to international stocks within your remaining stock portfolio.

You decide.

In the end, the choice is yours: when it comes to a sweet spot for foreign investments it depends on how well you can ignore the noise of the media and stay the course toward your individual goals. No matter how you choose, remember to diversify, be patient and verse yourself in a little investing history to keep perspective.

These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that the stated results will be replicated. Indexes are not available for direct investment but reveal positive and negative performance over time. Their performance does not reflect the expenses associated with the management of an actual portfolio. Diversification does not ensure a profit or protect against a loss in a declining market.

Copyright © 2012, Granite Hill Capital Management, LLC.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.