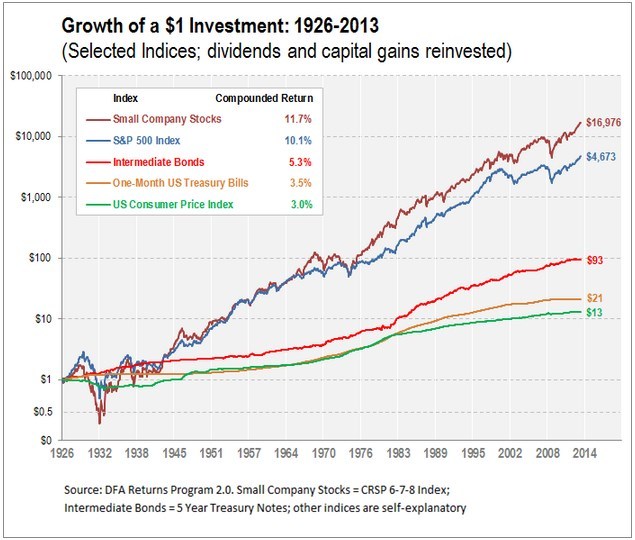

The growth of a $1 investment chart, a touchstone for many in the investment advice business, is a source of investment wisdom:

- Stay the course through the ups and downs.

- “When it comes to investing for your long-term goals, through history’s ups and downs, there’s nothing like stocks.”1

- “…the predominant trend for common stocks has been upward. Investors should consider this historical perspective when contemplating asset allocation decisions.”2

Seemingly sound advice. But as you prepare for, or settle into, retirement, it’s worth taking a closer look. Is there even more to this chart than meets the eye?

Managing risk and returns.

Clearly the compounding of returns over time has translated into large differences of accumulated wealth. Our eyes are drawn to the maroon line which illustrates how $1 invested in small company stocks at the beginning of 1926 grew, with all dividends reinvested, to nearly $17,000 by the end of 2013. This growth far surpassed the large companies of the S&P 500 and dwarfed the growth of intermediate bonds and one month Treasury-bills.

So why not pile all of your assets into the loftiest asset class based on historic growth? Because this also entails tolerating higher amounts of risk that the asset class may not deliver as expected or within a desired timeframe.

Facing setbacks along the way.

Periodic declines of stocks do not look frequent or gut-wrenching in the growth chart except for dramatic losses at the beginning of the Great Depression. In reality the declines are frequent and can be gut-wrenching.

On average, a bear market in the S&P 500 occurs every 3.5 years.3 Sometimes the declines occur quickly, such as the two months in September and October 1987 when stocks fell nearly 30%. At other times, they can be lengthy. The losses in the bear market beginning September 1929 lasted 34 months. As far as impact, the typical bear market loss of 18.8% translates to a loss of $188,000 on a $1 million stock portfolio.

As the Growth of $1 chart illustrates, if you can ride out these losses, you can expect to capture market returns over time. But if time isn’t on your side, it’s important to manage your portfolio accordingly, to avoid being trapped by bad timing.

Recognize the difference between paper and realized loss.

What many do not realize is that panicking and “getting out” because stocks have declined can penalize your returns if getting back in occurs after prices recover. Over the past ten years, Morningstar calculates that investor returns, which account for actual dollar flows into and out of funds, were 2.5% below the buy and hold investment returns reported by fund companies.4

For example, in the last bear market after the S&P 500 had already declined about 40% in the fourth quarter of 2008, fund investors withdrew $64 billion5 from domestic stock funds. During 2009, they withdrew another $29 billion,5 but the S&P 500 was up 26% for the year!

So, be cautious about using the chart to justify a heavy allocation to stocks without a plan for inevitable declines. “Staying the course” can be hard.

Taking a global view with your portfolio.

As 19th Century naturalist Alexander von Humboldt expressed, “The most dangerous worldview is the worldview of those who have not viewed the world.” Even if you are fully aware of and prepared for potential declines, remember the growth of a $1 chart provides only U.S. investment results. Blessed with many good fortunes, from not having a war fought on our home turf to an economic system that rewards innovation, creativity and hard work, U.S. investments during the past 88 years have done relatively well.

But consider these words:

“There is an obvious danger of placing too much reliance on the excellent long-run past performance of US stocks. The New York Stock Exchange traces its origins back to 1792. At that time, the Dutch and UK stock markets were already nearly 200 and 100 years old, respectively. Thus, in just a little over 200 years, the USA has gone from zero to almost a one-half share of the world’s equity markets.” — Elroy Dimson, Paul Marsh and Mike Staunton, Credit Suisse Global Investment Returns Yearbook 2013

We hope and expect that our nation will continue to thrive but long-term returns may not be as high as in the past. For this and other reasons related to diversification, it pays to invest internationally:

- Diversifying internationally: “Is it safe?”

- International Stock Allocation: 0%, 20%, 50%, or None of the Above?

What to do?

- Strike a balance between the growth of stocks and safety of bonds suited to your situation and time horizon.

- Stay the course by establishing preset rebalancing boundaries for when to buy and sell investment for maintaining your target allocations. Having rules in place to guide your way can help you avoid succumbing to emotional angst over short-term market noise.

- Diversify globally in a competitive world where market returns are found in the U.S. as well as beyond our borders.

If you need help crafting an investment plan designed accordingly, call or email for a complimentary discussion.

1 “A Case for Common Stocks,” Ave Maria Mutual Funds

2 “The Historical Case for Stocks—Growth of $1 Over Time,” Huntington Funds

3 To qualify as a bear market, cumulative monthly losses (looking backwards) must equal at least -10%. They end at the most negative cumulative loss. For example in the last financial crisis, the bear market began with a 4.2% decline in November 2007 and stayed in the red another 16 months until February 2009 when it reached a maximum negative cumulative loss of -51%.

4 Russel Kinnel, “Mind the Gap 2014,” Morningstar.com, February 27, 2014.

5 Investment Company Institute, “Summary: Estimated Long-Term Mutual Fund Flows Data (xls),” March 5, 2014

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.