Following the global financial crisis of 2008, the Federal Reserve Board took unprecedented steps to prevent bank failures, insure credit availability, and stimulate recovery. These successive bouts of “quantitative easing” fanned inflation fears as we experienced depressed interest-rate levels last seen in the 1950s.

We believe the Federal Reserve’s large-scale asset purchase plan (so-called “quantitative easing”) should be reconsidered and discontinued. We do not believe such a plan is necessary or advisable under current circumstances. The planned asset purchases risk currency debasement and inflation.” – Open letter to Fed Chairman Ben Bernanke signed by 23 economists, fund managers, and political strategists, 11/15/2010

Those most fearful of the threat of hyperinflation piled into gold in 2008 and 2009. But, contrary to their expectations, inflation averaged only 1.7% during the year ending in June 2013. In the four years prior to the 2008 recession, it had averaged 3.2%. After four-and-a-half years, their entire inflation protection rationale has yet to be validated.

So what gives? Will a long-awaited resurgence in inflation reignite gold? Will gold decline further and enter a period of dormancy as it did after the surge of the 1970s?

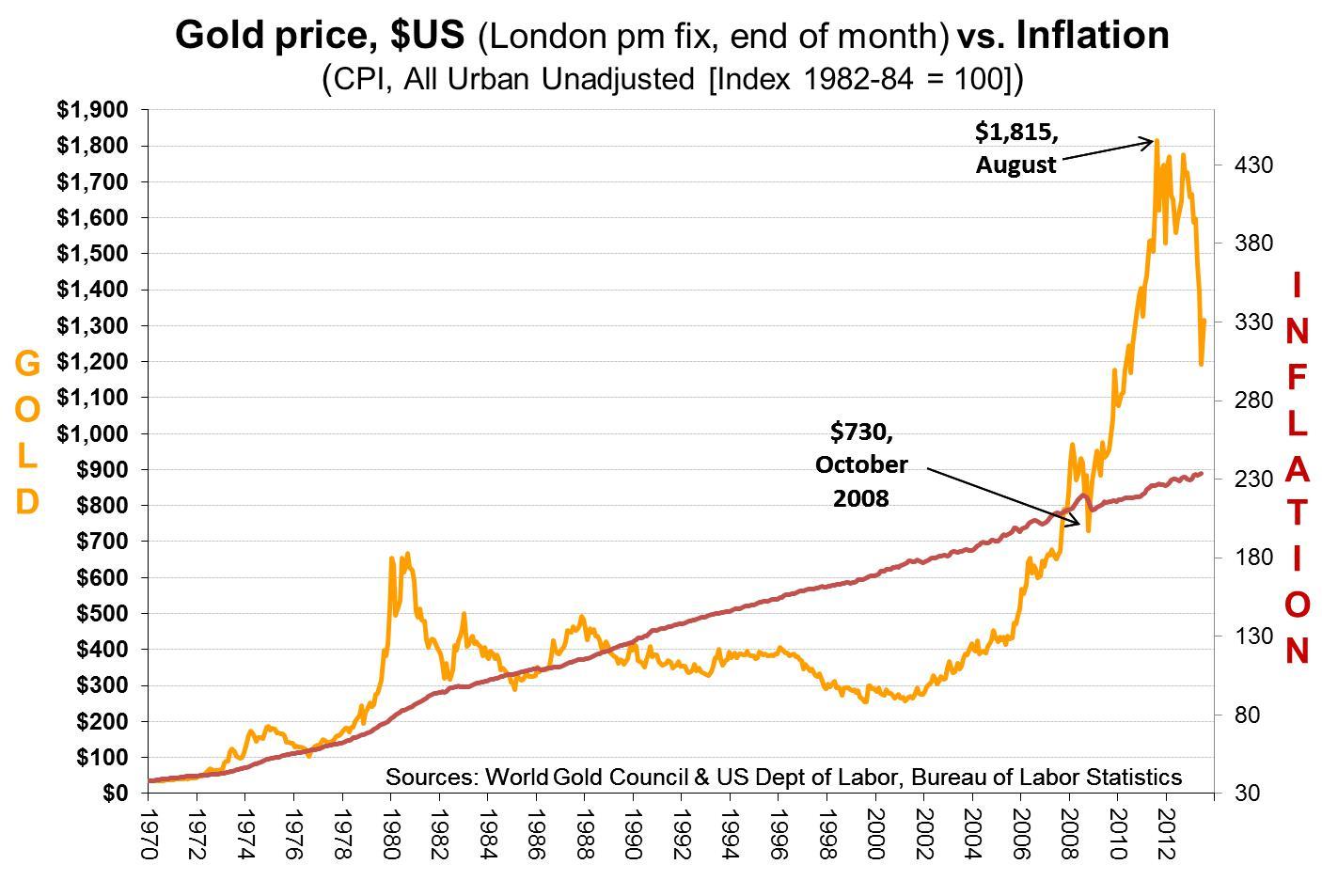

Claude Erb and Campbell Harvey address many rationales for owning gold in The Golden Dilemma. At a glance, the chart below seems dazzlingly compelling. But on closer analysis, the initial impression begins to lose its luster.

What does past inflation tell you about gold prices? Not much. If gold is an inflation hedge, as commonly believed, then its appreciation should offset rising consumer prices. In March 2012, when Erb and Harvey used inflation as the sole determinant of gold prices since 1975 (when US gold ownership became legal), they estimated the 2012 price should have been about $780 per ounce—about where CPI appears on the graph above and about $400 below the current price. Rather than rising in accordance with inflation, gold has lagged far behind in some decades.

What does gold supply and demand tell you? Again, very little. From World Gold Council estimates over 2001–2011, Erb and Harvey conclude production remains high, jewelry use has declined by a third, industrial and dental use has increased only slightly, and investment demand has quadrupled to nearly equal jewelry demand.

With just a click of the mouse substantial quantities of gold have been purchased through exchange-traded funds (ETFs). The SPDR Gold Trust, the largest ETF, stores physical gold in HSBC’s London vault as collateral. While investors had amassed more gold in this ETF than is held in the reserves of the Chinese central bank, some decided to click on “sell” this year. Rising prices normally curb demand but not so for gold investors in recent years. Erb and Harvey surmise momentum may be at play (where investors buy high and sell higher), as it was for Internet stocks during the tech bubble and housing prior to 2008. It remains uncertain at what price supply and demand return to equilibrium when momentum is washed out.

What is the bond market telling you about inflation and the need to hedge? Subdued inflation views continue to call into question the original motivation of using gold as an inflation hedge. A forward-looking estimate of inflation is provided by the difference between interest rates on TIPS (bonds whose interest payments fluctuate with inflation) versus regular fixed-payment bonds. This difference, a break-even inflation rate, indicates inflation will average 2.2% for the next 10 years, which is very close to the May 2013 estimate of 2.3% made by the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters.

Fearing inflation after easy money.

“The consequences of printing money over time will be inflation, [it’s] just difficult to predict when. If you’re looking for a hedge against potential inflation in the future and have a longer-term view, gold is an important part of anyone’s portfolio.” – John Paulson, billionaire hedge fund manager at July 17, 2013 CNBC/Institutional Investor Delivering Alpha conference.

Warren Buffett is also concerned about the consequences of quantitative easing, believing it is likely to be “very inflationary.” But he steers clear of gold because, as a non-productive asset, it produces neither dividends nor interest. Buffett would prefer to place his bets on productive businesses. High inflation may result, or not. Nobody really knows.

What is clear? It’s no wonder gold has been a poor inflation hedge. It’s a single, undiversified investment whose demand springs from those who need adornment and those driven by momentum investing. Recent extreme fluctuations in gold prices, even in the absence of inflation, make it appear as a variation of a Keynesian beauty contest where it is best to ignore your own view of beauty and instead concentrate on what other investors will perceive as beautiful. This form of speculation is difficult (and expensive) to play, as comments in Barron’s magazine reveal:

“We are living in a world of money printing. … That is why I have to recommend gold again. … Once gold surpasses $1,800 an ounce, it will run to the low-to-mid $2,000s.” — Felix Zuelauf, Zuelauf Asset Management. January 21, 2013.

“Investors can choose between artificially priced financial assets or real assets like oil and gold, or to be really safe, cash. … My first recommendation is GLD – the SPDR Gold Trust.” — Bill Gross, PIMCO. February 2, 2013.

“I am recommending gold, as I have done for many years. I will continue to do so until the gold price hits the blow-off stage, which is nowhere in sight. … The environment for gold couldn’t be better. … Gold could go to $5,000 or even $10,000.” — Fred Hickey, The High-Tech Strategist. February 2, 2013.

There is beautiful evidence demonstrating the effectiveness of building and adhering to a low-cost, globally diversified portfolio suited to your needs. In the face of that durable evidence, allocating a portion of your investments to speculative gold seems like a fool’s errand.

Photo credit for gold bullion and coins: Flickr user BullionVault

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that the stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Indexes reveal positive and negative performance over time. Because the size and variety of stocks and bonds in the marketplace is so large, indexes are used as models to depict, or simulate, the performance of selected groups or asset classes composed of stocks or bonds. Copyright © 2013, Granite Hill Capital Management, LLC.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.