Sources: International Monetary Fund, Global price of WTI Crude [POILWTIUSDM], retrieved from FRED, Federal Reserve Bank of St. Louis https://research.stlouisfed.org/fred2/series/POILWTIUSDM, March 25, 2016. January and February prices from U.S. Energy Information Administration, Crude Oil Prices: West Texas Intermediate (WTI) – Cushing, Oklahoma Online Data Robert Shiller, S&P 500 Composite, U.S. Stock Markets 1871-Present and CAPE Ratio

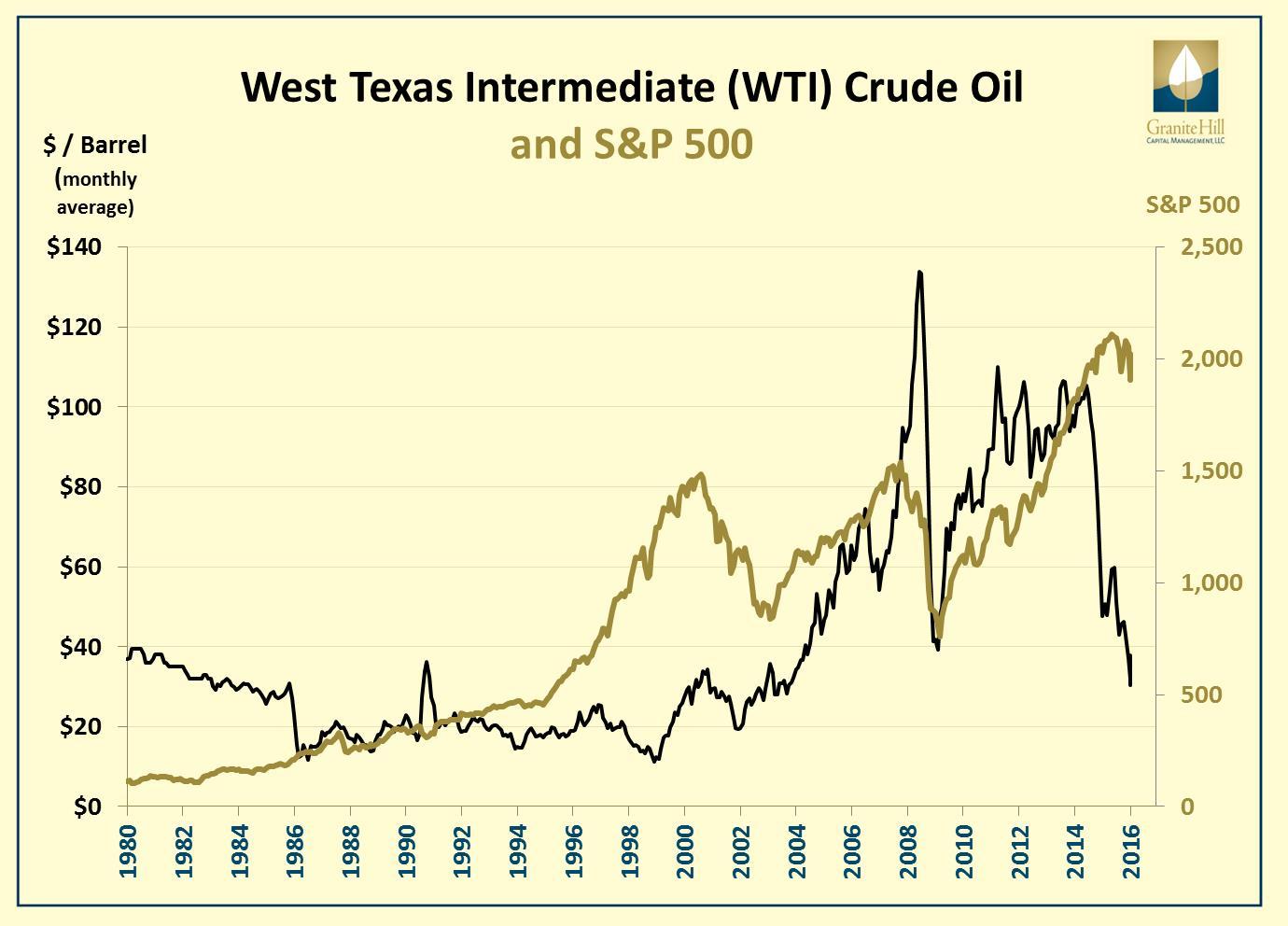

The relationship between crude oil and the stock market has commanded significant attention over the past few months. As oil prices rise, so do oil stocks. When oil falls, stocks fall. Many commentators, article writers, and researchers have taken note of this tendency. The Wall Street Journal noted the relationship in “Oil, Stocks at Tightest Correlation in 26 Years” and Former Federal Reserve Chairman Ben Bernanke examined it in “The relationship between stocks and oil prices.” Likewise, Dimensional Fund Advisors (DFA) wrote “Crude Oil and Financial Markets.”

To decipher the truth, we surveyed the findings of Bernanke and DFA and concluded that the current positive correlation between crude oil and stocks is a distraction and is best ignored.

The relationship between crude oil and the stock market has commanded significant attention over the past few months. As oil prices rise, so do oil stocks. When oil falls, stocks fall. Many commentators, article writers, and researchers have taken note of this tendency. The Wall Street Journal noted the relationship in “Oil, Stocks at Tightest Correlation in 26 Years and Former Federal Reserve Chairman Ben Bernanke examined it in “The relationship between stocks and oil prices.” Likewise, Dimensional Fund Advisors (DFA) wrote “Crude Oil and Financial Markets.”

To decipher the truth, we surveyed the findings of Bernanke and DFA and concluded that the current positive correlation between crude oil and stocks is a distraction best ignored.

-

Do crude oil and stocks move together?

Broad stock market indexes have generally moved in the same direction as oil over the past five to ten years. Now a few relevant statistics. Correlation measures the relationship between two variables. Perfect positive correlation equates to +1.0 and perfect negative correlation equates to -1.0. In point of fact, Ben Bernanke found a positive correlation of .39 over the past five years. This is in line with DFA’s finding of .33 for US stocks returns (.37 for global stocks) over the past ten years. However, after going back to 1986, DFA found a near-zero correlation.

From an economic perspective, this positive correlation is somewhat surprising. When oil prices rise, consumers pay more for gas and other petroleum based products, leaving less income for other types of consumption. Lower consumption leads to lower corporate earnings and, ultimately, a lower stock market. Rising oil prices and a falling stock market is, by contrast, a negative correlation. Indeed, prior to the global financial crisis, the media was reporting negative correlations as the Cleveland Fed noted in “Do Oil Prices Directly Affect the Stock Market?”

“U.S. Stocks Rally as Oil Prices Fall” (Financial Times).

“Oil Spike Pummels Stock Market” (Wall Street Journal)

-

Is the drop in crude oil prices due to increased supplies, sluggish demand or other factors?

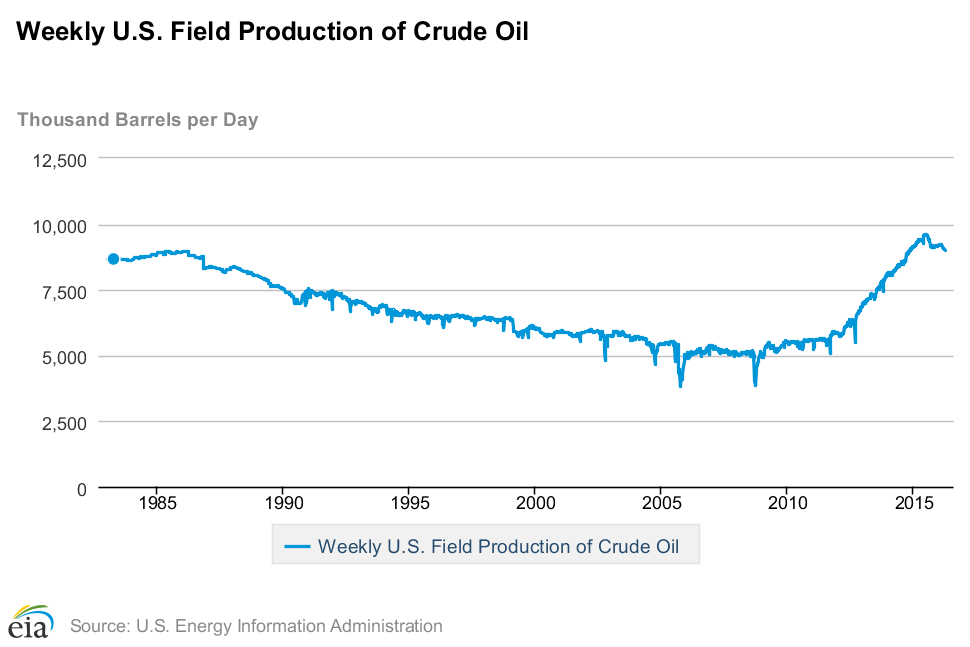

The dramatic increase in US oil production due to fracking is clear from the graph below. Other sources of increased supplies are well known too. The Saudi’s are continuously producing to maintain market share, in contrast to their past practice of cutting production to support prices. Likewise, in the aftermath of Iran’s nuclear deal, the country’s re-entry into global oil markets is assured, though quantities and timing are uncertain.

Oil demand is where there is a divergence of opinion.

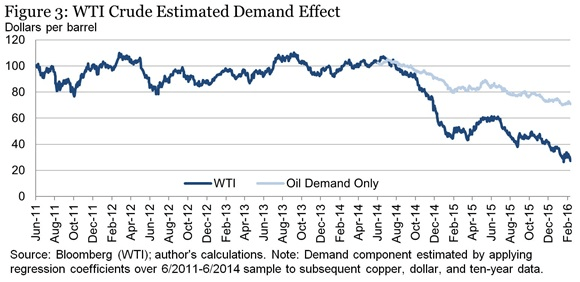

Bernanke believes that lower global demand has contributed to lower oil prices. He estimated oil would be trading at about $70 in mid-February, as seen in the light blue line on the graph below. This estimate assumed oil supplies remained constant since June of 2014. Instead, supplies increased and prices dropped much further, as shown in dark blue.

He also links weak stock prices to lower oil prices. Specifically, Bernanke writes that lower stock prices are “consistent with the idea that when stock traders respond to a change in oil prices, they do so not necessarily because the oil movement is consequential in itself, but because fluctuations in oil prices serve as indicators of underlying global demand and growth.”

By contrast, DFA reads the decline in oil prices as a result of increased oil supply, not reduced demand. They cite the following statistics:

US crude oil supplies climbed 36%, from 360 million barrels to 490 million barrels. They note that the clear increase in domestic production was offset somewhat by reduced net imports.

US refinery demand for crude oil is not slowing.

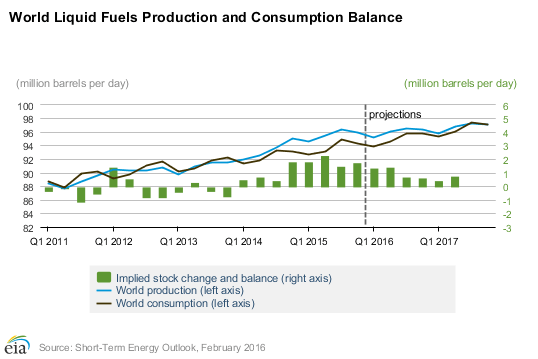

Whether the decline in oil prices is due to supply, or a combination of both supply and demand, can be debated. It is clear, however, that liquid fuel supplies have in fact increased. This results in lower prices. The “Implied stock change and balance” on the graph below illustrates increased supplies by using green bars.

-

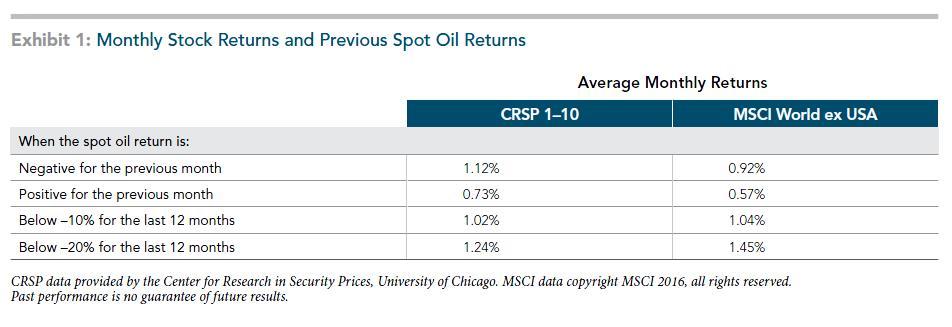

Do falling crude oil prices provide insight into stock performance the following month?

Oil traders incorporate supply and demand news into prices faster than a NutriBullet blender liquefies fruits and vegetables. Crude oil futures rallied 5% in mid-to-late February just because Venezuela merely reaffirmed that the oil producers meeting scheduled in mid-March would include Saudi Arabia, Russia, and Qatar. Never mind that the meeting was postponed. Stock and bond traders are no different when reacting to the news.

Given the speed of traders, it would be surprising to learn that oil price changes in one month had an impact on stock returns the following month. Indeed, DFA found “no evidence that falling oil prices predict declining stock markets.” Instead:

- Stocks rose, on average, the month following an oil price decline. Total US stocks (CRSP 1-10) and global stocks ex-US (MSCI World ex USA) rose on average 1.1% and .9%, respectively, the month following a decline during the period between 1986 and 2015. When oil climbed the previous month, stocks only rose .7% and .6%, respectively, on average.

- When oil declined a steep 10% from the previous year, stocks rose on average 1% per month.

- Likewise, when oil prices fell a steep 20% from the previous year, stocks performed even better. Perhaps this is evidence that lower oil prices can have a stimulatory effect on the economy and stocks. Consumers spend more and the net impact on business costs and profitability is overall positive.

Source: Dimensional Fund Advisors, Crude Oil and Financial Markets.

Source: Dimensional Fund Advisors, Crude Oil and Financial Markets.

Should you adjust your portfolio due to the strong positive connection between oil and stocks?

In our preface, we concluded that the positive correlation between oil and stocks over recent time periods was a distraction and best ignored. Indeed, correlations change over time and arguments for both positive and negative correlations exist. When confronted with such ambiguity, it is best to leave your portfolio alone.

One of our recommendations in “The Long-Run Damage of a Short-term Investment Approach” makes the argument quite well:

- Managing fund costs and other expenses.

- Allocating your holdings according to the fundamental drivers of performance, which includes accepting appropriate levels of market risk to reflect your need for commensurate reward.

- Diversifying your holdings globally to minimize the risk you must take on as you seek market returns.

- Locating your investments for tax-efficiency.

Always remember, successful investing requires tuning out the media.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.