Today, stock prices are fairly high while growth is widely expected to be slow. Should equity owners sell? I did, prior to the crash of 2008, and I now regret my decision every time the market hits a new high. I’m also afraid to get back in. It’s difficult to time the market, even if behavioral finance teaches us that the price is not always right.– Laurence B. Siegel, The Inventor of Behavioral Finance Looks Back (A book review of Richard Thaler’s Misbehaving: The Making of Behavioural Economics).

Stories of those who panicked and sold stock holdings during the 2008/09 global financial crisis are all too common. Wealth reductions of 30%, 40%, 50% and more were simply too much to stomach for many investors who sold when fear got the better of them.

What makes Siegel’s admission, quoted above, remarkable is not that he sold a portion of his stock portfolio — hubcaps and entire wheels were coming off as hedge funds, Bear Stearns, and AIG failed or collapsed in 2007 and early 2008 — but that he reveals that he did not get back in with what he took out. You don’t hear those stories much; they require more honesty than most people can muster.

Market timing is alluring and seemingly feasible.

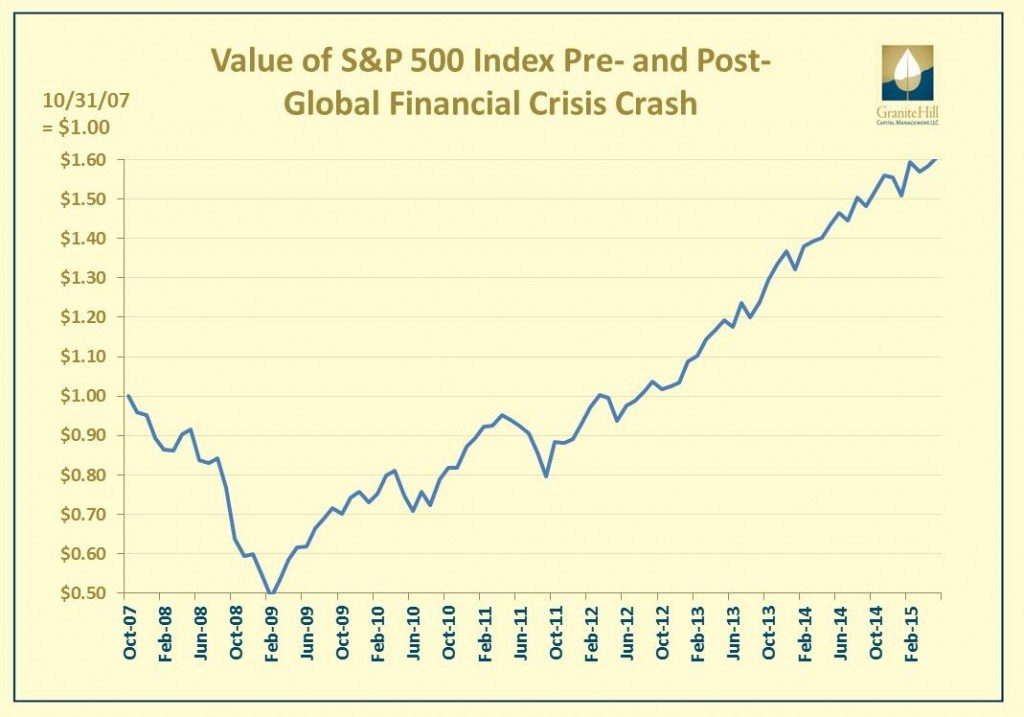

To be sure, sidestepping the 2008/09 crash by deviating from a target asset allocation towards safe assets turned out to be wise. A $1.00 investment in the S&P 500 at the end of October 2007 fell to less than 50 cents by February of 2009, but is now worth $1.60 as of the end May 2015. Regret in these circumstances is understandable.

Indexes are not available for direct investment but reveal positive and negative performance over time. Dividends and interest are reinvested but taxes are not considered. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Navigating the market’s ups and downs seems a possible feat, especially given the number of market timing newsletters and Wall Street market forecasts. Yet both have abysmal prediction records:

- In a study of 100 market timing newsletters over the five-and-a-half years since October 2007, only 25% beat a buy and hold strategy, although “none of them did so by getting out at or near the top and getting in at or near the bottom.” (So, How Did the Market Timers Do? Mark Hulbert, Barron’s March 12, 2013)

- A review of S&P 500 annual performance forecasts from the past few years for major Wall Street firms revealed that the average forecast deviated from actual results by as little as 6.4% and as much as 21.4%. (A deeper analysis of the causes and motivations behind such varied ranges is provided by PunditTracker.)

Successful market timing requires not only knowing when to sell, but also when to get back in.

This requires considerable mental flexibility and leads away from the sound investment strategy of diversification.

The riskiest moment is when you’re right. That’s when you’re in the most trouble, because you tend to overstay the good decisions. So, in many ways, it’s better not to be so right. That’s what diversification is for. It’s an explicit recognition of ignorance. And I view diversification not only as a survival strategy but as an aggressive strategy, because the next windfall might come from a surprising place. I want to make sure I’m exposed to it. – Peter Bernstein interview, Jason Zweig, MONEY Magazine

The tools of market timing are crude.

Take the popular Shiller ratio or CAPE, built upon the behavioral finance notion that stock prices overshoot or undershoot fair value by wide margins because investors are far from rational. It appears to predict the significant losses that occurred during the ten years following peaks in 1929, 1966, and 1999. In reality its predictive power is not this precise, as we noted in Shiller PE indicates weak stock returns: investors should remain strong. And now even the originator of the ratio is not relying upon it:

I’ve been very wary about advising people to pull out of the market even though my CAPE ratio is at one of the highest levels ever in history. Something funny is going on. History is always coming up with new puzzles. – Robert Shiller, The S&P 500 P/E Ratio Is 19, Unless It’s Actually 27.

A three-step market timing alternative.

Hopefully these practical and psychological challenges to market timing persuade you it is a bad strategy. So what’s the alternative?

- Acknowledge that with high stock valuations come lower future returns but no one knows the path to those lower returns or even how high those valuations might be. Saving more, working longer, and/or consuming less may be prudent actions for a more secure retirement.

- Create a plan with well-diversified investment allocations that you can stick with through thick and thin. This plan should reflect both your resources (investments, future earnings, and other assets) and goals.

- Rebalance your allocations to stay on target. This approach forces you to sell your safe-harbor holdings and buy stocks when fear is rampant—a strategy we previously addressed in this post: Rebalancing during “traumatic market events”- the whole or half the story?

If you’d like to further discuss our process for creating a solid plan and keeping your allocations on track, call or email us today.

This blog entry is distributed for educational purposes and should not be considered tax, investment or financial advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that the stated results will be replicated. Performance does not reflect the expenses associated with the management of an actual portfolio. Copyright © 2015, Granite Hill Capital Management, LLC.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.