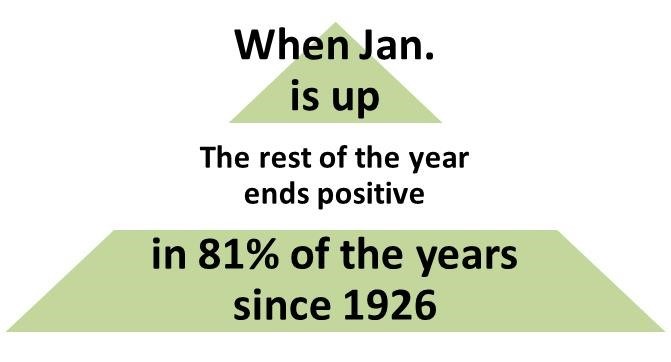

January’s 5.6% gain makes the rest of the year looks bright according to the January indicator.

The logic of the January indicator, according to aficionados, is as follows:

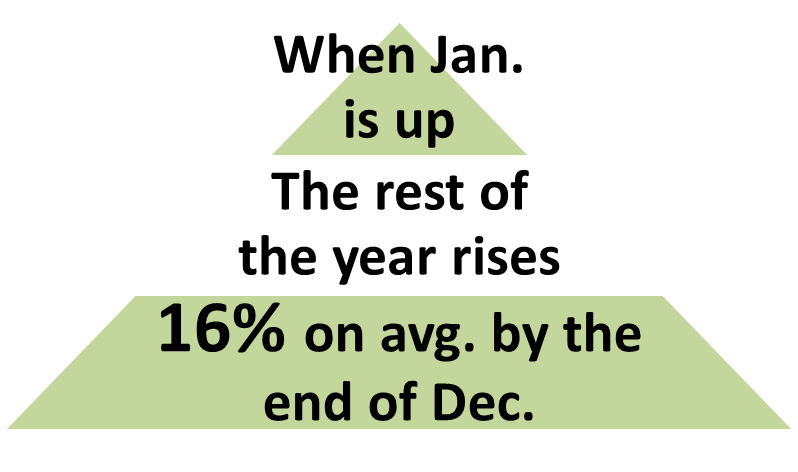

And the payoff for the rest of the year appears rich:

But can high odds of a rich payoff result from such a simple forecasting method?

Yes, according to a Wall Street technician who was quoted recently in Barron’s, “… the historical ‘facts and figures’ are what they are. The data is the data.“

We love data and history so let’s look at all the data to see whether the indicator is valid and has merit for making investment decisions.

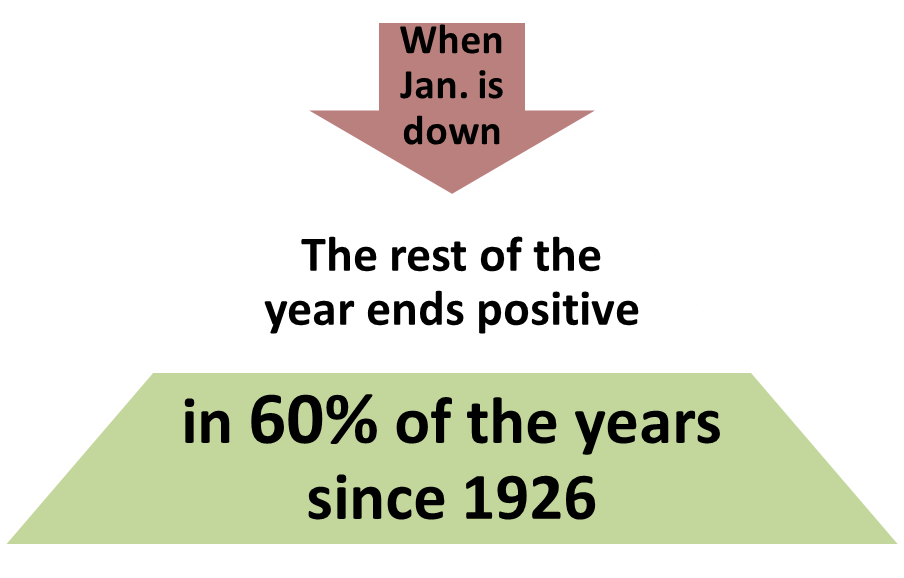

First, what are the odds when S&P 500 performance is down in January?

As a method to increase your odds of identifying bad performance, the January indicator fails. Even when January’s performance is down, odds are 60% the S&P 500 will be up by the end of the year.

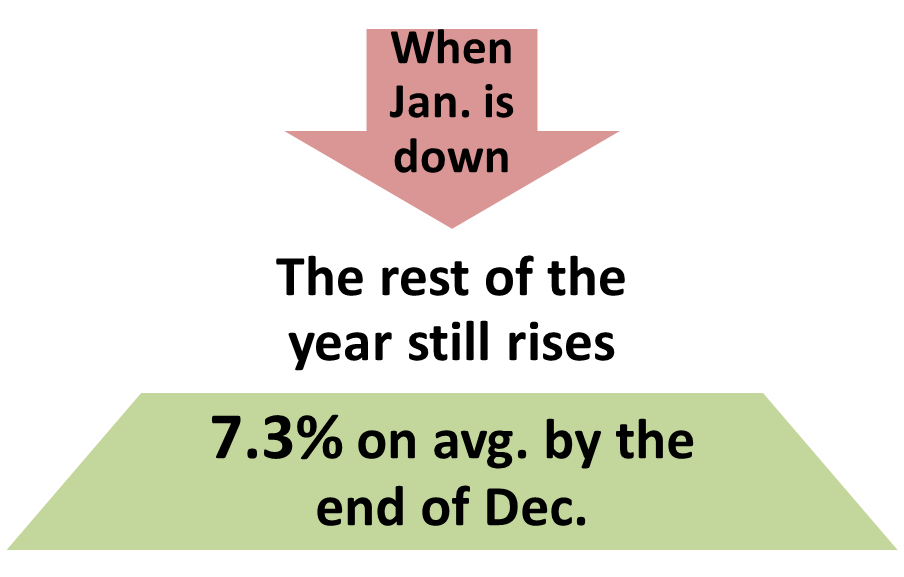

Second, what about performance for the rest of the year when the S&P 500 is down in January?

While performance is less than half of what it is when January is up, 7.3% is still healthy.

A granular look at the data reveals four reasons the January Indicator is misleading and should be ignored.

S&P 500 Index data provided by Standard & Poor’s Index Services Group.

Past performance is not a guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

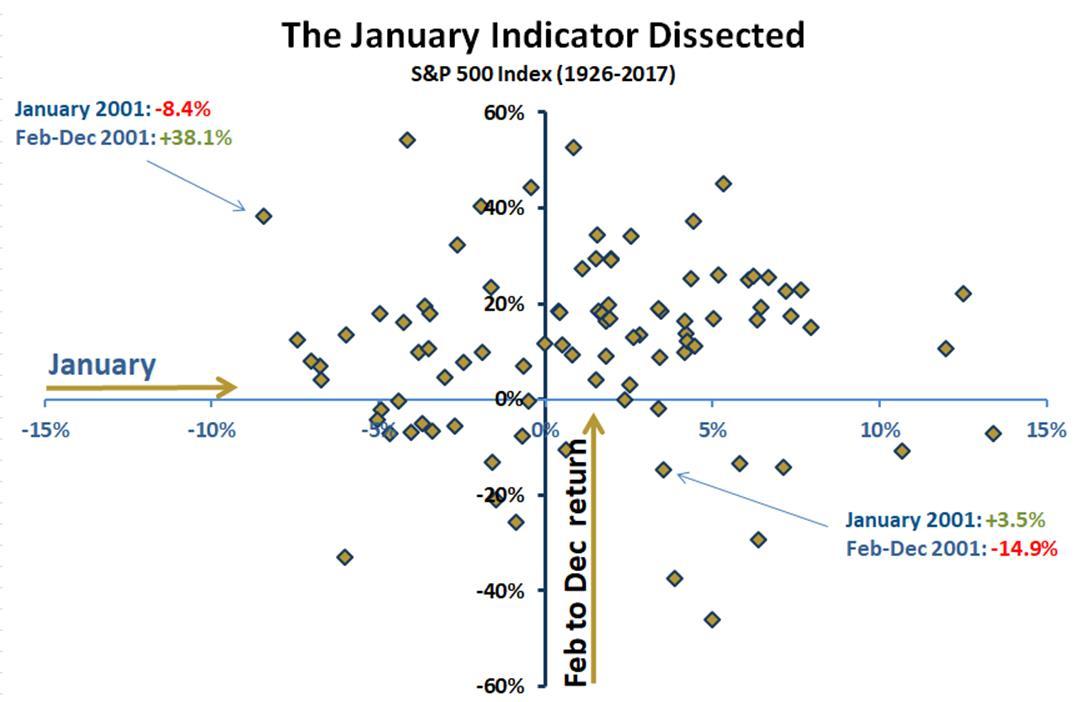

- January’s performance offers no predictive insight into the rest of the year. The scatter plot of diamond points represents various combinations of performance in January versus performance in the rest of year. It is more of a shotgun effect than a trending pattern. Geek note: a regression equation shows the coefficient of determination (R squared) is 0.1%.

- Focusing on short-term performance can lead to lost opportunities. For example, in January 2016 when the S&P 500 lost -5.0%, the S&P 500 was up 17.8% by the end of December. If the January indicator was interpreted as a signal to reduce exposure to stocks or completely sell out, the rebound would have been missed. Likewise, the declines in January of 8.4% and 3.6% in 2009 and 2010, respectively, would have led to missed gains of 38.1% and 19.4%.

- Averages obscure risk. Even when January’s performance is positive (the right side of the scatter plot), sharp declines by the end of the year are possible. The worst outcome occurred when the S&P index rose 5.0% (horizontal axis) in January of 1931 but lost 46% by the end of December (vertical axis). More recently, the S&P 500 rose 3.5% in January 2001 but fell 14.9% by the end of December.

- The January indicator runs counter to patience. Warren Buffett thoughts on patience and short-term forecasts were captured in a previous post:

“Lethargy bordering on sloth remains the cornerstone of our investment style.” – 1990 letter to Berkshire Hathaway shareholders.”

“We have long felt that the only value of stock forecasters is to make fortune-tellers look good. Even now, Charlie (Munger) and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.” – 1992 letter to Berkshire Hathaway shareholders.

At first glance, the January indicator might have appeal. It certainly is easy to understand. But the four reasons noted above shed light on why it should be ignored. Rather than trying to beat the market based on hunches, headlines, or indicators, we believe a disciplined, long-term approach using evidence vetted in the academic community yields better odds of success.

This blog entry is distributed for educational purposes and should not be considered investment, financial, or tax advice. Investment decisions should be based on your personal financial situation. Statements of future expectations, estimates or projections, and other forward-looking statements are based on available information believed to be reliable, but the accuracy of such information cannot be guaranteed. These statements are based on assumptions that may involve known and unknown risks and uncertainties. Past performance is not indicative of future results and no representation is made that any stated results will be replicated. Indexes are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Links to third-party websites are provided as a convenience and do not imply an affiliation, endorsement, approval, verification or monitoring by Granite Hill Capital Management, LLC of any information contained therein. The terms, conditions and privacy policy of linked third-party sites may differ from those of this website.